Buyer Side

Purchase Invoice Financing supports procurement by helping pay supplier invoices first, so cash can be preserved for other operating needs.

Trade and cashflow support

Trade financing helps Singapore businesses manage supplier payments, unlock cash from receivables, and provide payment assurance when dealing with customers, suppliers, landlords, project owners, or government agencies.

Import, export, and assurance

Trade financing is useful when a business needs to pay suppliers before sales proceeds are collected, give customers longer payment terms, or provide a guarantee that contractual or payment obligations will be met.

Purchase Invoice Financing supports procurement by helping pay supplier invoices first, so cash can be preserved for other operating needs.

Sales Invoice Financing advances cash against unpaid customer invoices before the buyer makes payment.

Banker's Guarantees and Standby Letters of Credit provide payment or performance assurance to beneficiaries.

For buyers and importers

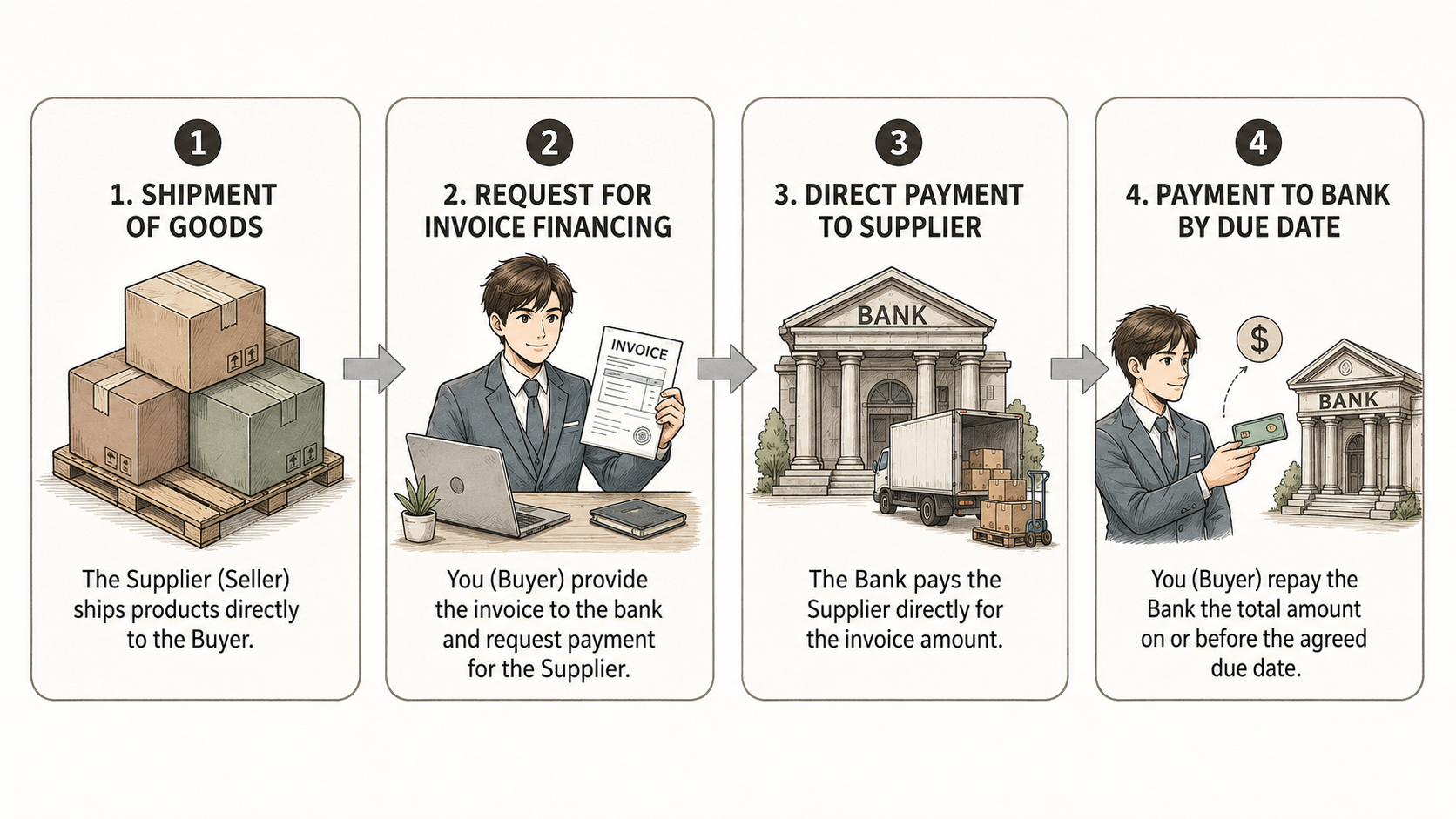

Purchase Invoice Financing helps a business finance local or overseas procurement of goods or services. The bank may pay supplier invoices first, and the borrower repays the financing amount plus interest later.

It can free up working capital that would otherwise be tied up in payables, supporting inventory purchases, project fulfilment, and supplier relationships.

Certain bank facilities may finance up to 100% of supplier invoice value for open account trade, subject to facility approval and bank terms.

For sellers and exporters

Sales Invoice Financing helps unlock cash from receivables by providing an advance on unpaid invoices before the buyer pays. This can help businesses offer customers payment terms without carrying the full cashflow strain.

It supports businesses that have delivered goods or services but need liquidity before customer collection, especially where sales are on credit terms.

Certain bank facilities may advance up to 90% of invoice value for domestic and cross-border open account sales, subject to bank assessment.

Payment and performance assurance

A Banker's Guarantee or Standby Letter of Credit helps reassure a beneficiary that payment or contractual obligations will be met. These facilities are commonly used when a counterparty needs stronger assurance before awarding a contract, extending credit terms, releasing goods, or accepting a tender.

A bank undertaking to pay the beneficiary if a valid claim is made according to the guarantee terms. Common use cases include lease agreements, contract agreements, project tenders, bid bonds, and performance bonds.

A payment commitment used in domestic or cross-border transactions, where payment is made when the documents or demand specified in the SBLC are presented.

Choosing the right structure

Consider Purchase Invoice Financing when your business needs stock, goods, or services before customer cash is collected.

Consider Sales Invoice Financing when invoices have been issued and you need cashflow before buyer payment is received.

Consider a BG or SBLC when a beneficiary needs a bank-backed commitment for payment, tender, performance, lease, or contract obligations.

Ready to structure your trade facility?

Speak with us to review your trade cycle, customer terms, supplier requirements, and financial documents before approaching lenders.

Contact usNo-obligation assessment

Please prepare the following documents so we can evaluate your eligibility.

FAQ

Trade financing in Singapore covers: Letters of Credit (LC), which provide a payment guarantee from a bank to a seller upon fulfilment of documentation conditions; Trust Receipts (TR), which allow importers to receive goods before full payment while the bank holds a security interest; banker's guarantees (BG) for trade commitments; invoice or receivables financing for exporters awaiting payment from overseas buyers; and supply chain finance programmes. The right structure depends on your trade flow - whether you are an importer, exporter, or both - and the payment terms with your overseas counterparts.

A Letter of Credit (LC) in Singapore trade finance is a bank commitment to pay a seller provided the seller meets specific documentary conditions. It protects both parties - the seller is assured of payment, and the buyer controls payment conditions. A Trust Receipt (TR) is a post-shipment facility where the bank releases goods documents to the importer while retaining a security interest until the importer repays the bank. Typically, an LC is used before goods arrive, and a TR bridges the period between receiving goods and collecting receivables from customers.

Some trade financing facilities in Singapore can be extended on an unsecured basis for established SMEs with a strong trading track record and banking relationship. In practice, many banks require a combination of the company's financial standing, existing credit limits, and the quality of underlying trade instruments before extending unsecured trade lines. The EFS Trade Loan provides government risk-sharing and can make it easier for Singapore SMEs to access trade financing lines they might not otherwise qualify for on their own.

Documents required typically include: confirmed purchase orders or sales contracts from overseas buyers or suppliers, commercial invoices, shipping documents (bill of lading, airway bill, or packing list), and the company's standard financial and KYC documents (corporate bank statements, financial accounts, ACRA profile, NRIC of directors). For LC applications, specific documentation instructions are embedded in the LC terms. Incomplete or inconsistent trade documents are a common reason for delays, particularly for first-time applicants.

The EFS Trade Loan is a government-backed trade financing facility helping Singapore SMEs manage import, export, and overseas project cash flow needs. EnterpriseSG shares a portion of the credit risk with participating financial institutions - making lenders more willing to extend trade lines to SMEs that may not meet standard bank credit thresholds. The facility can be used for trade-related working capital including inventory purchases, pre-shipment financing, and overseas contract fulfilment. Eligibility criteria mirror other EFS products - Singapore-registered, at least 30% local equity, and meeting the relevant SME criteria.

Yes, though first-time importers or exporters may find the initial application more involved because lenders have no prior trade history to assess. Banks typically want to see a confirmed order, a creditworthy buyer or supplier, and a clear understanding of the trade cycle. Beginning with a smaller trade finance facility - even a trust receipt line for one or two shipments - can help build a track record that supports a larger, more flexible trade financing relationship over time.